There’s a financial equivalent to a superpower that can totally transform your modest savings and contributions into a substantial personal fortune one day…it just works silently and consistently in the background.

Compounding interest is often called the 8th Wonder of the World, originally described this way by Albert Einstein, and for good reason. This epic concept has the potential to turn even small, consistent savings into life-changing wealth.

I’m going to take you on a trip into what I feel is the base understanding for all things investment. We'll break down how this financial magic works, why it's so powerful, and how you can use it to build your own wealth strategy.

What is Compounding Interest and How Does It Work?

The Basic Mechanics of Compounding

Compounding interest is like a financial snowball that grows larger and faster as it rolls down the hill of time.

Unlike simple interest, which calculates returns only on your principal amount, compounding calculates returns on both your original investment and the accumulated interest from previous periods.

“This means your money doesn’t just grow – it grows exponentially.”

Now, let's break down how this works…

Imagine you invest a cool $1,000 with an annual return of 7%. In the first year, you'll earn $70. But in the second year, you're not just earning 7% on your original $1,000 – you're earning 7% on $1,070.

This might seem small initially, but over a few years, then decades, the difference will blow your mind.

The Time Factor: Why Starting Early Matters

Time’s the most crucial ingredient in the compounding recipe. The earlier you start investing, the more time your money has to grow. Consider two scenarios:

A client of mine, let’s call her ‘Sandy’ (out of respect for her preference to remain anonymous), starts investing $200 monthly at age 35, continues until he's 65 (so 30 years of contributions)

Result = $415,858 (based on a 10% annual return…calculator here)

VS

‘James’…starts investing $200 monthly at age 25, continues until he’s 35 (so only 10 years of contributions), SAVES $40,291, then just lets it fly until age 65…

Result = $703,053 (based on a 10% annual return…calculator here)

Surprisingly, even though English contributed for a shorter period, he ended up with a ton more for his nest egg due to the extra years of compounding.

This shows the incredible power of cracking into this early, just time work its magic.

Moral of the story? Get anyone you know who’s young to start dripping it in TODAY!!! It’s time in the market that counts the most.

Practical Strategies to Maximise Compounding (without the fluff)

To truly leverage compounding interest, consider these strategies:

Start investing as early as possible

Choose investments or KiwiSaver funds with consistent, reliable risk vs returns history (click to understand what this is)

Reinvest any monetary giftings, dividends or returns

Be patient! and avoid withdrawals!

Increase your contributions over time as your salary increases

The Psychology of Compounding

Compounding isn't just a mathematical concept – it's a mindset.

It requires discipline, patience, and you need to shift your mindset to thinking long-term instead of the fleeting ‘spending my profits as they arrive’ approach.

So many people struggle with compounding because it doesn't show results straight away.

The magic happens in your later years when your savings start to grow exponentially.

Real-World Examples of Compounding POWER

Let's look at some more scenarios:

$5,000 invested annually at 7% return for 40 years could grow to approximately $1,142,920!

$500 monthly investments with a 8% annual return could reach around $1,356,278 after 40 years!

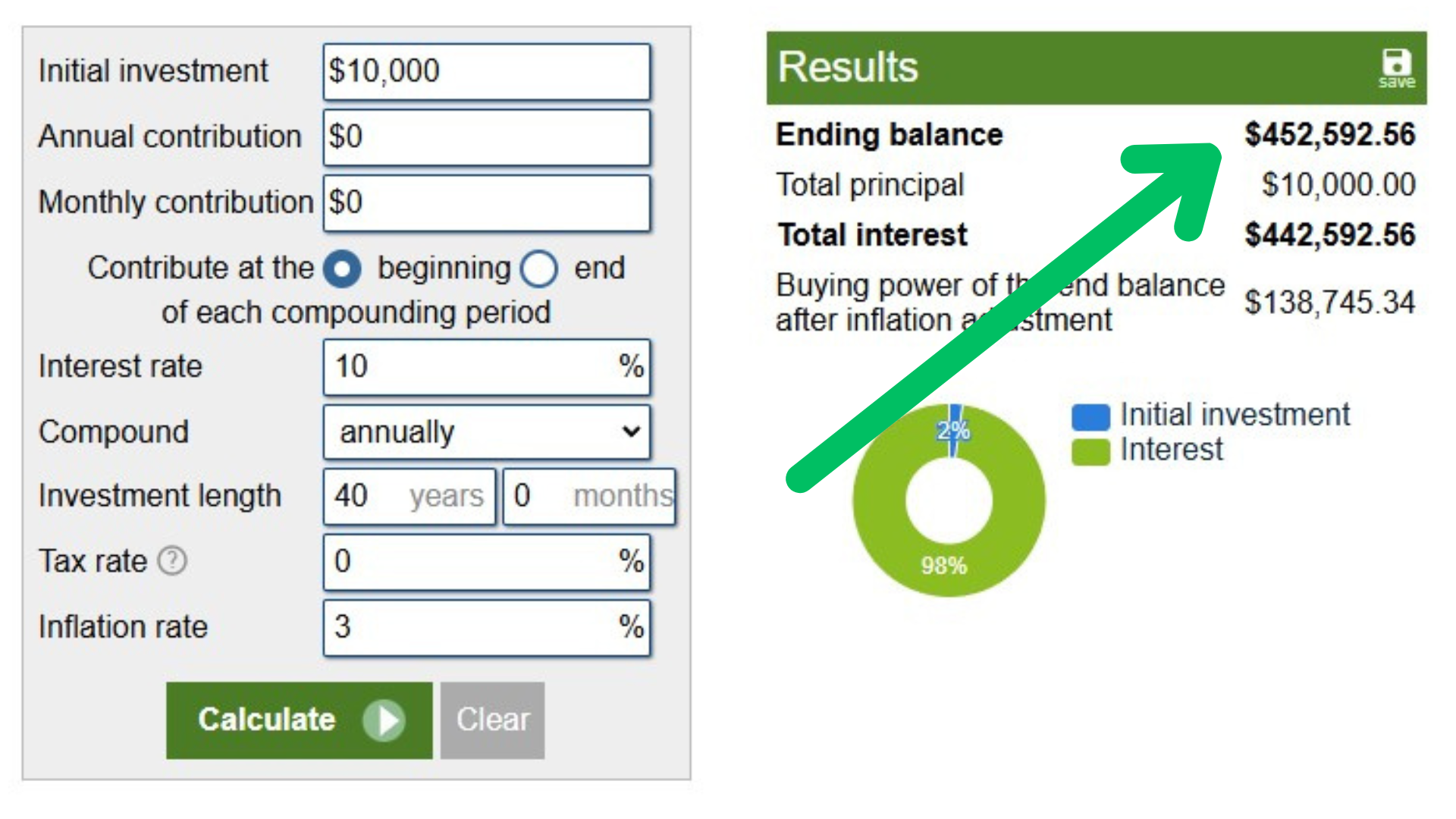

A one-time $10,000 investment at age 25, left untouched until retirement, could grow to over $450,000!

Potential Pitfalls to Avoid

While compounding is powerful, be aware of:

Market volatility

Inflation

Inconsistent investing

Spending your profits

Tools and Resources for Compounding Success

Retirement calculators (click here)

Investment tracking apps (click here)

Financial planning software (click here)

Robo-advisors (if you like average results)

Conclusion

Compounding interest is your best financial strategy mate – it's the most important concept in the financial world.

By understanding and implementing these principles, you can achieve that cushy future that seems so out of reach at first glance.

Remember, the best time to start investing was yesterday, the next best time is now.

FAQs

Q: Is compounding interest guaranteed?

A: No, compounding returns depend on the performance of your investments. While historical market returns provide a guide, future performance is not found in a crystal ball.

Q: How often does compounding occur?

A: Compounding frequency varies – it can be daily, monthly, quarterly, or annually, depending on the investment type.

Q: Can compounding work with small amounts of money?

A: Damn straight! Even small, consistent investments or contributions can grow significantly over time. That’s exactly what you KiwiSaver is doing.

Q: What's the difference between simple and compound interest?

A: Simple interest calculates returns only on the principal, while compound interest calculates returns on both the principal and accumulated interest.

Q: Are there risks involved with compounding investments?

A: Yes, all investments carry some risk. Diversification and a long-term perspective can help mitigate these risks. Seek advice to avoid the pitfalls and add more to your nest egg.

P.S. I’m a believer that life is subtly pointing us in the direction we should go, but it’s up to us to actually listen.

Hope this helped!

Chris George | Personal Finance Adviser

Want more…?

👉This video explains how to WIN the financial game!📝

👉This video explains how a couple could accumulate an extra $1,200,000 in Kiwisaver over the next 25 years, without increasing their contributions or risk 📈

👉This video explains how to stop your income and life insurance premiums go up💡

👉Let's sit down and figure out how to map out a future you can look forward to…Click here or below to schedule a strategy call.

Note: Any information provided is for general and educational informational purposes only and is not personalised advice. Your circumstances are unique and there’s no templated road to a cushy retirement! For personalised advice, please book a Strategy Call.