The role of life insurance is to protect the financial progress you've achieved so far, and ensure that future plans can stay on track where health or injury issues arise. This area of financial planning is considered the backbone of your financial retirement plan.

The term 'Life insurance' includes monthly disability covers such as income or mortgage and business disability covers, plus lump sum covers such as trauma, major trauma, tpd and life. These covers all serve different purposes in your protection plan.

Generally, for most situations, a spread of these covers is the best approach if your budget allows.

We believe in protecting what you’ve spent so many years building with advanced personal insurance strategies that stand the test of time.

This video will help you understand how to calculate the amount of cover you’d need to prevent financial upset should a health or injury event occur.

This video reveals how to achieve the cover you need, without over-paying the insurance company.

Self-Insuring Versus Outsourcing Insurance

When we analyse what insurance cover, amounts and cover structures are appropriate, we must first take into consideration what resources and/or assets you have to 'self insure' if a situation arose.

This is the planning part of protection planning. We then outsource the area's you cannot self-insure to an insurance company.

Generally, the younger you are the less resources and/or assets you have available so there is more insurance needed.

Additionally, the younger you are, the less likely you are to claim so the premiums are cheaper.

Generally, the older you are the more resources and/or assets you have available so less insurance is needed.

Additionally, the older you are, the more likely you are to claim so the premiums are more expensive.

Whatever your age, we start by setting a plan, then work out the best insurance plan to fit your plan, then find a balance between the ultimate plan and an affordable plan that meets budget.

Scenarios To Analyse

When analysing your life insurance needs, it's appropriate to assess two scenarios to each household.

The scenario of a critical illness or injury preventing you from being able to earn or for 'home executive' roles, being able to keep the home kept.

The covers that assist you in this event are monthly disability covers such as Income or Mortgage covers, Trauma cover and Total Permanent Disability (TPD) cover.

The second scenario is when an earner or home executive passes away or is diagnosed terminally ill.

The cover that assists you in this event is Life cover.

Therefor, we need to establish the plan for the two scenarios.

We back up what you cannot support yourself through your own assets and resources with insurance cover from specialist providers.

Note:

We don't factor in health cover to the above two scenarios as health cover is not designed to assist your financial situation with a monetary benefit.

Life Insurance Claim Statistics

It's important to know the likelihood of finding yourself in these scenarios.* This helps you make an informative decision on what cover types are priority for your budget.

For a male non-smoker during his working years (age 18-65), the chance of:

a temporary disability lasting more than 6 months is 10%

becoming permanently disabled is 4%

suffering from a critical illness is 17%

passing away is 9%.

For a male smoker during his working years (age 18-65), the chance of:

a temporary disability lasting more than 6 months is 9%

becoming permanently disabled is 4%

suffering from a critical illness is 32%

passing away is 17%.

For a female non-smoker during her working years (age 18-65), the chance of:

a temporary disability lasting more than 6 months is 19%

becoming permanently disabled is 4%

suffering from a critical illness is 11%

passing away is 6%.

For a female smoker during her working years (age 18-65), the chance of:

a temporary disability lasting more than 6 months is 18%

becoming permanently disabled is 4%

suffering from a critical illness is 25%

passing away is 12%.

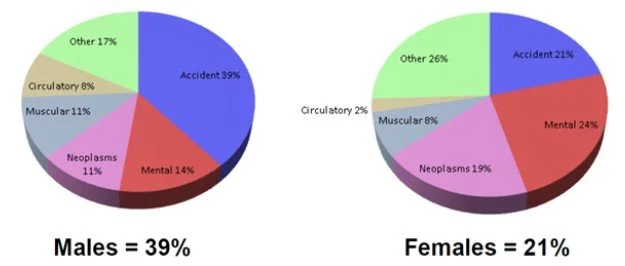

Income Protection Claims (Reasons for inability to work)

Gender differentiated reasons for loss of earnings claims with Asteron Life.**

Notes:

**Statistics sourced from Quotemonster. New Zealand's largest risk insurance rating agency.

**Statistics sourced from Gen Re income protection claim statistics. Gen Re is New Zealand's largest re-insurer.

Notes:

**Statistics sourced from Quotemonster. New Zealand's largest risk insurance rating agency.

**Statistics sourced from Gen Re income protection claim statistics. Gen Re is New Zealand's largest re-insurer.

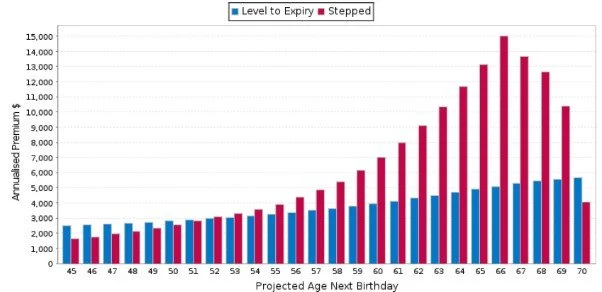

Premium Types

The type of premium is a very important consideration for the sustainability of your protection plan. From 1:30 to 8:45 of the video explains the basics for the different types of premiums and when to use them.

Level Premium

If your Lifetime Cashflow projections display you being able to retire in more than 10-15 years, you are under the age of 50, and your budget allows, it often makes sense to consider a level premium for the cover that replaces income or associated costs of an illness.

This is to ensure that your premiums for that type of cover remain affordable for that period of time so you aren't having to reduce or cancel cover through the ages you most need it and is cumulatively a cheaper way to buy the cover. We often structure Mortgage, Income, Trauma and Major Trauma covers with a level rate.

The below example displays $7,500 p/m Loss of Earnings cover for a male non-smoker. The cumulative difference between level and stepped premium is $65,139.

Stepped Premium or Yearly Renewable Term (YRT)

If your mortgage cash flows project you paying down your debt, I will usually suggest a stepped premium for covers like Life and TPD that often have the majority purpose of paying down debt.

If the purpose of the cover is to reduce debt, the benefit amounts for these covers should be reduced with the debt balance over time. This results in a 'level-like' premium and is cumulatively a cheaper way to buy the cover.

Between 8:45 and 10:20 of the video explains further.