The below concepts are intended for educational purposes only, and are not personalised advice.

Macro Economic Basics

Understanding the basics of how the financial world works on a macro level is the key to your success of accomplishing your financial objectives.

I've included the following videos to watch which will educate you on the fundamental concepts to consider along your journey. This video is made by Ray Dalio, founder of one of the worlds largest fund managers, Bridgewater Associates.

Is Kiwisaver A Type Of Investment Fund?

Kiwisaver is a type of managed fund. Managed or investment funds are mutual funds or exchange-traded funds in which the portfolio managers make investment decisions. Kiwisaver as a product, enforces strict retirement savings while also benefiting from government and employer (if applicable) contributions. Your Kiwisaver fund cannot be liquidated until you turn age 65 unless you suffer from a permanent disability or extreme financial hardship. The advantage is that it will provide a strict savings plan.

In comparison, a normal managed fund only benefits from your direct contributions but can be accessed and/or liquidated at any point without penalties. There may be a small administration fee for withdrawal.

Dollar Cost Averaging

Dollar cost averaging (DCA), is an investment strategy where you regularly invest a fixed amount of money at set intervals, regardless of market conditions.

By doing this, you can benefit from both high and low market prices over time, reducing the risk of making poor investment decisions based on short-term fluctuations. DCA is a long-term approach that aims to smooth out market volatility and promote consistent investing.

Overall, dollar cost averaging offers a systematic and disciplined investment strategy that aims to remove the emotion and guesswork from investing, promoting consistency and long-term growth potential.

Compounding, The 8th Wonder Of The World

The underlying wisdom of the adage derives from the power of compounding, what Albert Einstein called the eighth wonder of the world. “He who understands it, earns it. He who doesn't, pays it,” he is said to have said.

Compounding is the process in which an asset’s earnings, from either capital gains or interest, are reinvested to generate additional earnings over time. This growth, calculated using exponential functions, occurs because the investment will generate earnings from both its initial principal and the accumulated earnings from preceding periods.

Compounding, therefore, differs from linear growth, where only the principal earns interest each period.

See this Blog we wrote to learn more: https://www.bridgefinancial.nz/blog/2025/2/15/the-8th-wonder-of-the-world

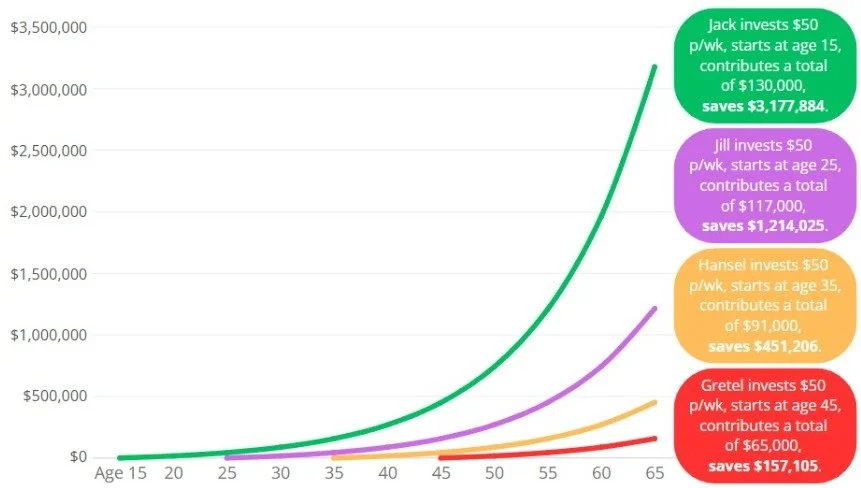

Investing Now Is Better Than Later

The markets are kindest to those who stay faithful to it longest.

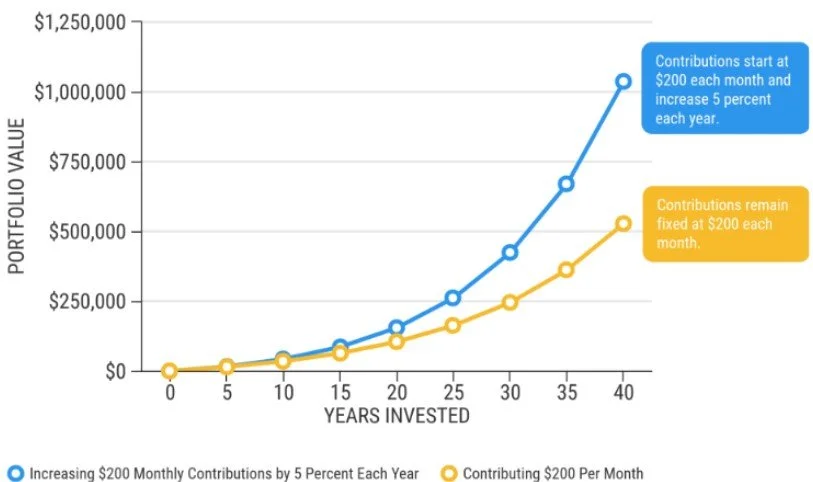

The Benefit Of Increasing Your Contributions

The below graph illustrates the potential difference in outcomes by steadily increasing your contributions over time at a rate of 5% per year.

Rate of Return

Rate of return is one of the most important factors that determine how much money you make investing.

The below examples show how a seemingly small difference in return can result in a large change in investment value over time.

For accurate modelling, we work with 'real rates of return'. A real return is the return percentage after inflation, fees and taxes are taken out. A nominal rate of return includes inflation.

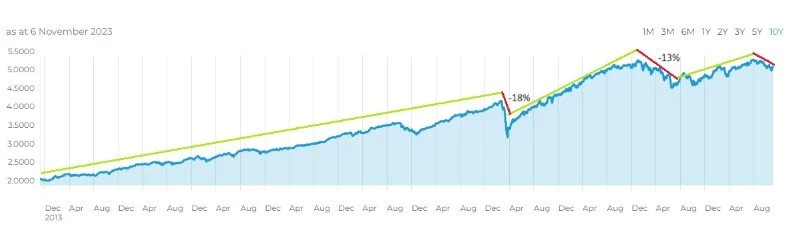

Downside Mitigation

An equity graph (below) visually displays a funds performance over time through different market cycles.

Growth phases and recessionary phases (known as drawdowns) are usually quoted as the percentage between the trough and peak or peak and trough.

Growth phases are represented by the green arrows in the below equity curve and represents the funds period of higher highs, or positive gains.

Drawdown phases are shown as the red arrows in the below equity curve. A bigger drawdown can mean the fund takes longer to recover from which means your money takes longer to get back to where it was.

Please read this article to understand how to protect your KiwiSaver and/or investments from large drawdowns: https://www.bridgefinancial.nz/blog/2025/2/8/ovkb61njtkwrz20fgchfsc0dh14za2

Diversification

Diversification is the process of spreading investments across different asset classes, industries, and geographic regions to reduce the overall risk of an investment portfolio.

Diversification aims to smooth out an otherwise volatile equity curve of a fund.

Please read this article for more: https://www.bridgefinancial.nz/blog/kiwisaver-and-investment-diversification

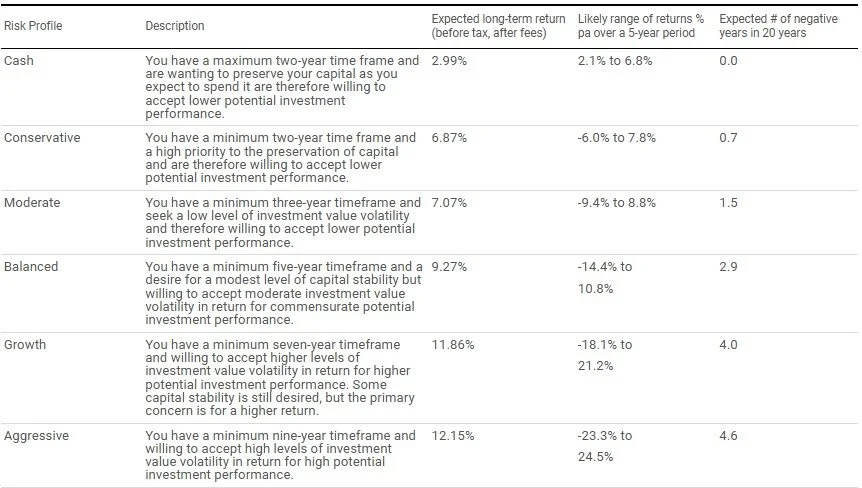

Investment Risk and Your Risk Profile

Investment risk has been defined as “the amount the value of a portfolio varies over time”. This means that the greater the expected variability or fluctuation in performance, the greater the investment risk. Risk may also be defined as the amount that the actual return differs from the expected return.

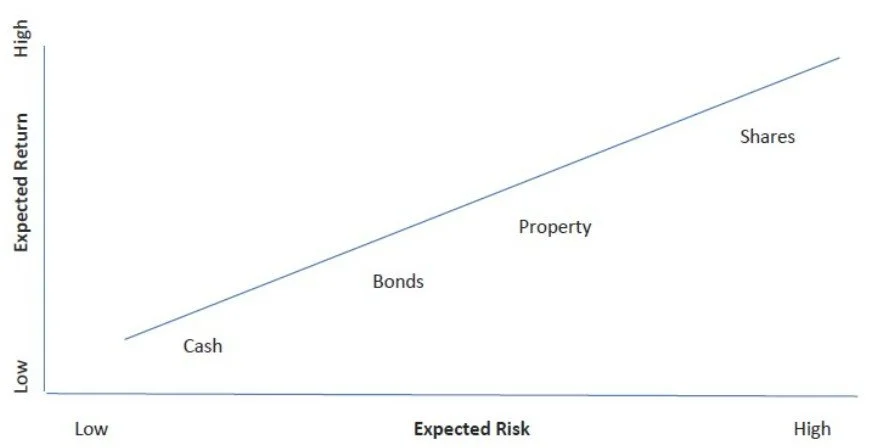

Risk versus Return

Income assets defined as cash and fixed interest investments where returns consist of interest payments and a repayment of capital as a future date. Growth assets include shares, property and alternative investments where returns are mainly from an increase in the capital value.

On a risk / return basis, income assets have lower returns and lower risks than growth assets. Investors wanting to earn higher returns generally have a higher proportion of growth assets in their investment portfolios; however risk increases as the proportion of growth assets increases.

The risk / return characteristics of the four asset classes are shown below:

Risk Profile

The objective of the risk assessment questionnaire is to ascertain your view on the risks you are comfortable to accept while aiming to achieve your investment objectives. The questions in the Risk Assessment Questionnaire focus on:

Time Horizon

Long Term Goals and Expectations

Short Term Risk Attitudes

The results provide your risk profile and this is used to identify the most suitable portfolio from the six profiles identified by Morningstar featuring differing levels of risk.

In general, most people are conversant with the concept of investment return, and understand, for example, that a 10% per annum return on $100,000 would result in $10,000 being received each year. However, many people do not clearly understand volatility, and the Risk Return Trade Off.

Volatility is a term that refers to the unpredictable upward and downward shifts of investment values over a period of time. The greater the volatility the more frequent the shifts. In the long term, the greater the volatility the higher the likely returns. It is your attitude towards this volatility combined with your time horizon that helps determine your risk profile.

To assist in the development of this strategy, we discussed your attitude to risk and your concerns in a number of areas.

Allocations

Funds can be grouped into five types of risk allocation, as below.

Your asset allocation can be established by ascertaining a) your personal risk aptitude and b) your age and stage of life, which is often dictated by how long you have until you plan to draw from the fund.

I suggest finding a balance of the two when deciding on your risk allocation.

Life Stages

As you move closer to accessing or liquidating your money, we want to slide your asset allocation towards defensive/conservation assets, reducing your exposure to more volatile assets such as the the share market, commodities and digital assets, and increasing your exposure to less volatile assets such as cash and fixed income assets. This creates less volatility and smaller drawdowns as you approach the end of your investment horizon.

For example purposes only, the orange line in the below diagram displays the allocation for a standard investment timeline and a standard personal risk aptitude. Until age 55 the allocation is kept in growth with around 80% of the funds in more volatile markets and 20% in less volatile markets. We then reduce the volatility exposure from age 55 to decrease risk leading up to retirement which in this example, is planned for age 65.

Active VS Passive Fund Management

Active fund management involves professional managers making active investment decisions to outperform a benchmark index.

Passive fund management aims to replicate the performance of a specific index, with minimal decision-making. Active seeks higher returns and carries higher fees, while passive offers lower costs and seeks market-level returns.

Note: The independent research article can be sourced here.

Fees

Fees are how the fund manager charges you for the work they do to grow your money. These types of fees are charged as a percentage of your fund balance and are withdrawn periodically by the fund management provider.

There is generally a base fee(s) that is applicable to the fund manager. This fee covers the various fund manager and adviser costs.

A portion of the adviser fee may be either additionally drawn or included. This varies with different providers.

The manager may also charge a performance fee charged that is only applicable if the fund beats it's benchmark performance.

There is a fee incorporated and/or additionally charged for personalised ongoing advice. This will be outlined in the disclaimer section at the beginning of this document if applicable.

Note: The fee for the recommended fund(s) can be found in the Product Disclosure Statement in the Appendix.

Returns

Additional to the points raised over the last few pages, I feel solid after-fee returns over all risk allocation strategies is a key element in choosing a reliable fund manager.

This is in contrast to only assessing returns for the risk allocation you are currently selecting.

Steady after-fee returns over all allocations shows the manager has an in depth understanding of all financial markets they're investing in and can adjust your fund appropriately as your age and life stages change over time.

Responsible Investment

Socially responsible investing is any investment strategy which seeks to consider financial return alongside ethical, social or environmental goals. The areas of concern recognized by SRI practitioners are often linked to environmental, social and governance topics.

This trend has been around for a long time, but initially struggled under the assumption that choosing to ethically tilt your portfolio would negatively impact returns. As time has gone by, further work in this area has evidenced that this is not the case. And arguably, companies with poor ethical records will often be avoided by consumers or suffer from expensive lawsuits.

Effectively, socially responsible investing, has become a day to day practice for every fund manager. However, some providers have had this as more of a focus in their business. These area's of concern are made of mainly:

Controversial weaponry, Tobacco, Civilian firearms, Gambling, Adult material, Fossil fuels, Alcohol, Environmental destruction, Human rights abuses, Armaments, Labour rights violation and Corruption.